How Open Banking is Transforming the Way Businesses Get Paid

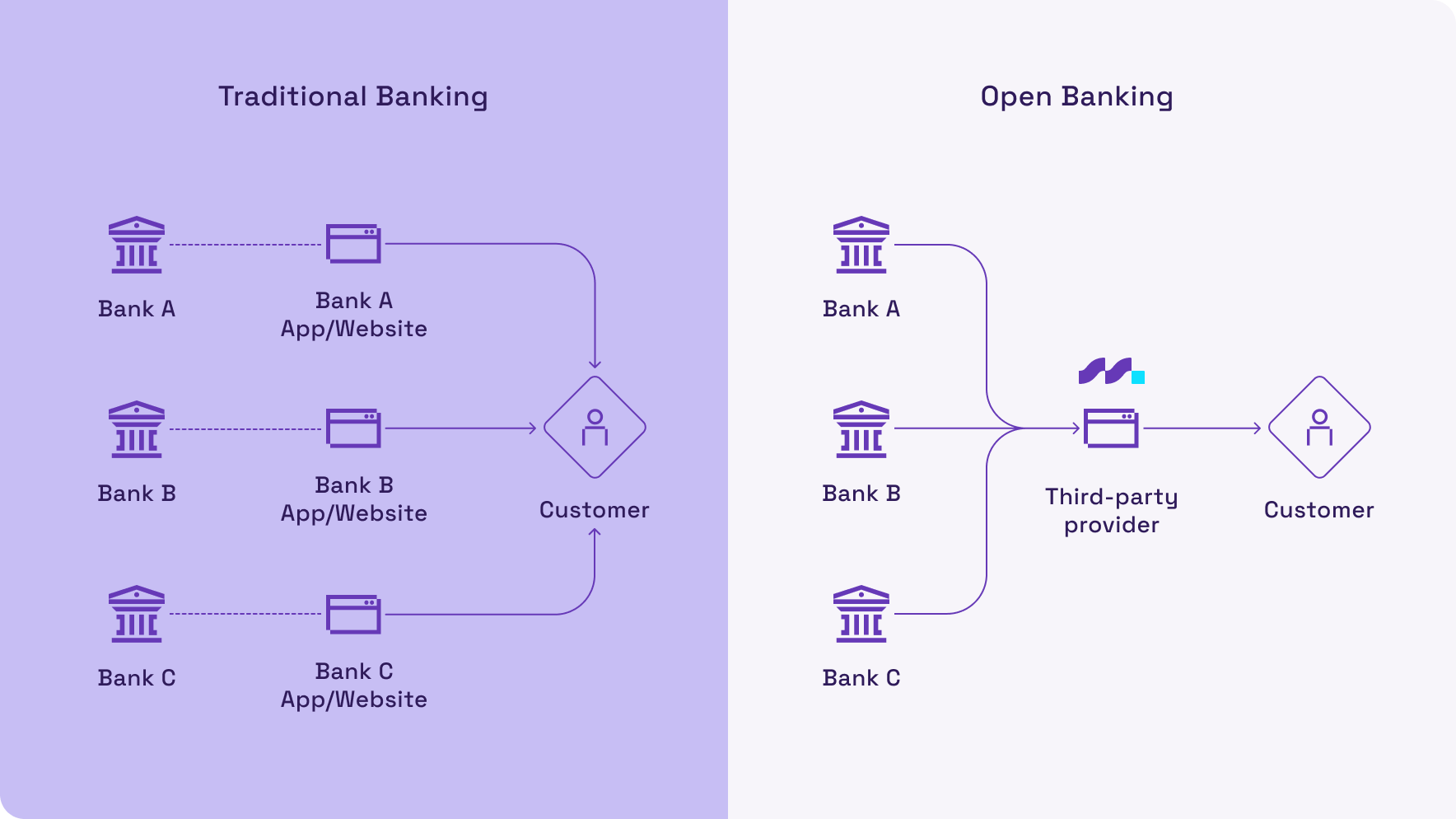

The tradition with payments has historically been one of ‘walled gardens’. A bank was a bank and moving money between institutions followed a very clear process, with businesses and individuals having little visibility into the mechanics of what happened between authorisation and settlement, let alone the data being gathered behind the scenes.

In recent years, what’s known as ‘open banking’ has begun to reshape that model. By allowing financial institutions to share customer-consented data through secure APIs, payments have shifted from being kept within closed, institution-controlled systems to interoperable ecosystems where businesses can build faster and more automated payment flows. The implications of open banking go beyond data access to potentially change what's possible at every stage of the payment lifecycle.

To share an example, think of OpenAI (the company behind ChatGPT), which operates on the principle of allowing third parties to take their existing infrastructure and build on top of it. In open banking, that means accessing financial data via APIs (with people’s permission1) in order to create new, user-friendly solutions.

What open banking actually enables

One of the more immediate impacts of open banking can be account-to-account payments with fewer intermediaries involved.

Rather than routing transactions through card networks with their associated fees, processing delays and chargeback exposure, open banking can enable funds to move directly between bank accounts. For businesses processing high volumes of payments, this can contribute to improvements in cost and speed of workflows and outcomes.

Authentication and consent can also improve. Instead of storing card details or relying on customers to manually enter payment information, open banking allows businesses to initiate payments through verified, consent-based flows that connect directly to a customer's bank account. This can help reduce fraud exposure, simplify compliance, and provide a more streamlined experience for recurring billing and direct debit arrangements.

Importantly for finance teams, open banking payments arrive with more detailed transaction data. Rather than a truncated reference and a BSB, structured, standardised information is provided. This opens the door to automated rather than manual reconciliation, which can help finance teams to keep pace as the business scales.

Open banking around the world

Australia is not the first market where open banking is available. Take a look at how it is leveraged around the world:

In the UK, open banking has been operational since 2018 and now facilitates over 11 million active users2 and millions worth of transactions each month. Variable Recurring Payments3, the UK's consent-based alternative to direct debit, are being rapidly integrated by businesses that need flexible, automated billing without the friction of traditional mandates. Meanwhile, merchants giving their customers the option of account-to-account4 (‘Pay By Bank’) payments can benefit from reductions in processing costs compared to card-based alternatives.

India's Unified Payments Interface5 links multiple bank accounts into a single smartphone app, merging several banking features, seamless fund routing & merchant payments in one place. As explained by the Federal Bank of India6, UPI allows instant, 24/7 interbank transactions and has been widely adopted, with over 100 banks offering UPI-based services. The infrastructure has become so ubiquitous that it has effectively leapfrogged card networks for a significant share of payments. More than 15 billion transactions7 were reportedly processed per month as of November 2024.

Singapore's PayNow enables instant transfers between participating bank accounts and e-wallets in Singapore using a mobile number, NRIC/FIN, or Virtual Payment Address (VPA). Users can send and receive funds without needing to enter bank account details.

Across all three markets, open banking has become an important part of the modern payment experience. As Australia's banking ecosystem matures, similar innovations are expected to play an increasingly important role in the local payments landscape.

The Australian opportunity

Australia's Consumer Data Right framework8 (which gives individuals the right to share their data between service providers of their choosing) and the continued expansion of PayTo are powering the shift to newer ways of transacting.

PayTo in particular can help bring Open Banking principles directly into the payment flow, enabling businesses to initiate real-time, pre-authorised payments from customer bank accounts with consent managed digitally rather than through paper mandates or traditional direct debit processes.

This creates a window of opportunity for first-movers in Australia. The companies that invest in building payment flows on top of real-time rails and open banking infrastructure will have operational and cost advantages that become increasingly difficult for competitors to replicate once the market matures.

The advantages of open banking for businesses include:

- Faster cash flow as payments settle in real time rather than waiting on batch cycles,

- Improved payment and tracking accuracy through rich data and automated reconciliation

- Simpler customer onboarding through consent-based flows that replace form-filling and account verification

- Reduced manual work for finance teams

- Enhanced customer experience because transactions are fast and easy

Building on the right infrastructure

Capturing the open banking opportunity typically involves the connection of real-time payment rails, reconciliation logic, and data flows into a coherent operational layer that finance and product teams can actually work with.

The good news is there’s no need for organisations to build a solution from scratch.

Monoova provides a single platform connecting NPP, PayTo, and automated reconciliation designed to deliver payment operations that are faster, more accurate, and built to scale.

Discover how Open Banking, PayTo and real-time payments can help your business improve cash flow, automate reconciliation and create better customer experiences.

Speak with a Monoova specialist today >>

FAQs

Q1: What is Open Banking?

A1: Open Banking allows customers to securely share financial data with approved providers through APIs, enabling new financial services and payment experiences.

Q2: How does Open Banking improve payments?

A2: Open Banking enables account-to-account payments, real-time transaction visibility, improved authentication and richer payment data.

Q3: What is the relationship between Open Banking and PayTo?

A3: PayTo applies Open Banking principles to payments, enabling real-time, consent-based payments directly from bank accounts.

Q4: What are account-to-account payments?

A4: Account-to-account payments move funds directly between bank accounts without relying on card networks or intermediaries. Infrastructure is helping drive Open Banking adoption across the financial sector.

2https://www.fca.org.uk/news/statements/fca-and-psr-set-out-next-steps-open-banking

3https://www.openbanking.org.uk/variable-recurring-payments-vrps/

4https://www.openbanking.org.uk/insights/pay-by-bank-a-big-step-forward-for-everyday-payment/

5https://www.digitalindia.gov.in/initiative/unified-payment-interface-upi/

6https://www.digitalindia.gov.in/initiative/unified-payment-interface-upi/

7https://www.bis.org/publ/bppdf/bispap152_e_rh.pdf

8https://www.cuscal.com/newsroom/articles/the-definitive-guide-to-open-banking-in-australia/

.png)

.png)